Invoice Discounting: A Complete Guide to Benefits, Process, and Risks

2025-09-26

Introduction

Every business, whether small or large, faces the same problem: customers often take weeks or even months to clear their payment. During this waiting period, companies still need to manage salaries, supplier bills, and other day-to-day expenses. This gap between sending an invoice and actually receiving the money can create real pressure on cash flow, making it harder for businesses to stay financially stable.

To handle this challenge, many businesses look for practical ways to access their locked-up funds without relying on traditional loans. One such method is invoice discounting, a financing tool that helps companies improve their cash flow by using unpaid invoices as a resource. It’s not about taking on new debt but about making existing earnings available sooner, giving businesses the flexibility to cover expenses and plan ahead with more confidence.

This article will break down how invoice discounting works, explore its benefits and risks, and highlight why it has become a trusted financing option across industries. Whether you’re managing late-paying clients or dealing with seasonal cash flow gaps, understanding this approach can give your business the financial flexibility it needs.

What is Invoice Discounting?

Invoice discounting is a way for businesses to get money quickly without waiting for customers to pay their invoices. Here’s how it works: when a company delivers a product or service, it sends an invoice to the customer. That invoice might have a payment term of 30, 60, or even 90 days. This means the business has to wait while its money is stuck in that unpaid bill. But during this time, the company still needs cash to pay salaries, buy raw materials, or cover daily expenses.

With invoice discounting, the business doesn’t have to wait. A finance provider offers the company most of the invoice value in advance, usually around 70% to 90%. When the customer finally pays the invoice, the finance provider returns the remaining amount after keeping a small fee for the service. In simple words, invoice discounting helps a business use the money it has already earned, just earlier than usual.

This method is not like taking a loan because the company isn’t borrowing new money. Instead, it’s getting quicker access to funds that already belong to it. That’s why invoice discounting is often considered safer and more flexible. To make this process easier, many businesses use e invoicing software. It helps them generate, track, and organize invoices in one place, ensuring everything is accurate and ready when they approach a finance provider. This reduces errors, saves time, and makes the whole discounting process smoother.

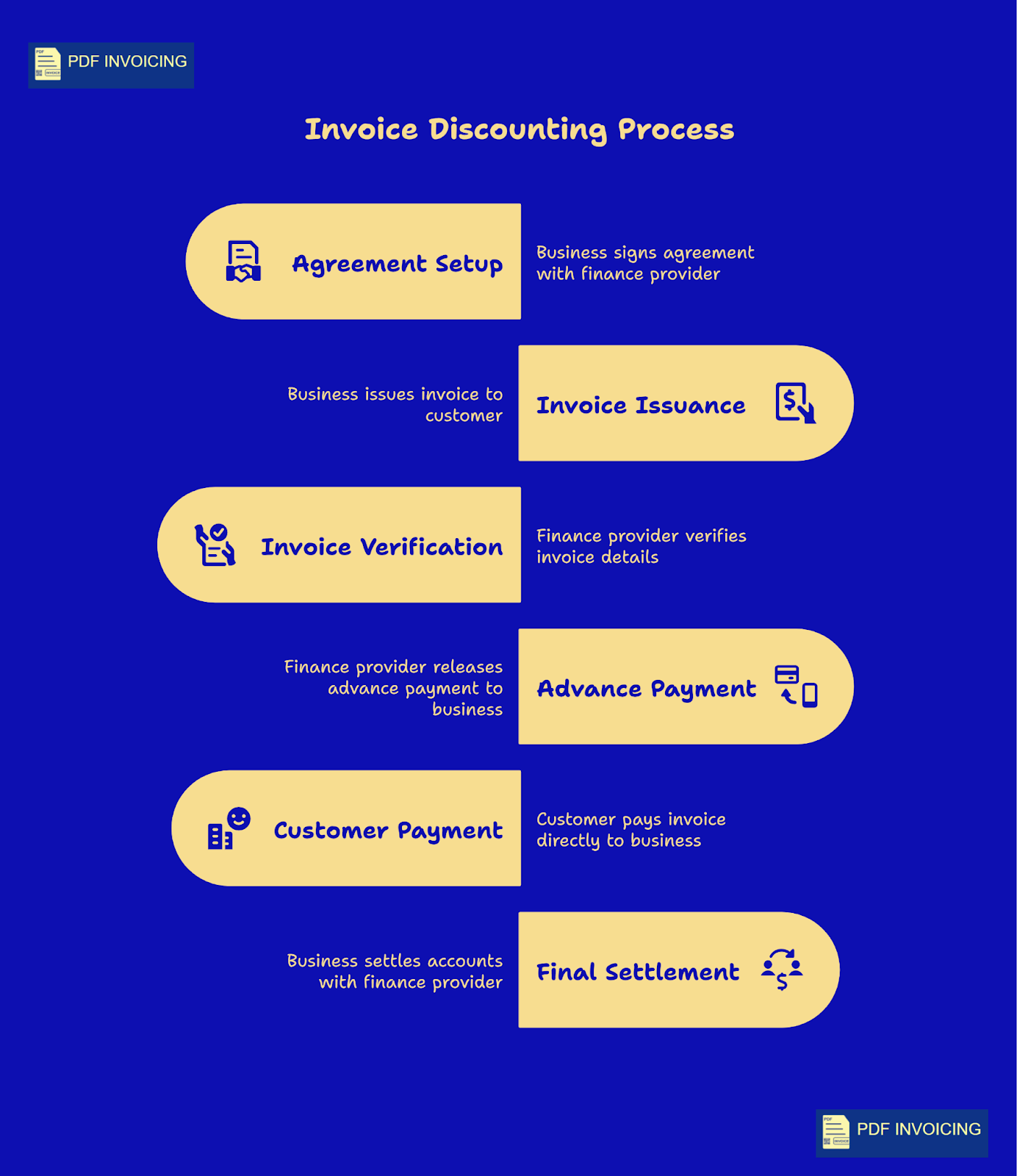

How Does Invoice Discounting Work?

Invoice discounting is a process where a business turns its unpaid invoices into quick cash. Two parties are involved: the business that needs funds and the finance provider who gives the advance. This way, the business doesn’t have to wait months for customers to pay and can still manage its daily operations smoothly.

Here’s a clear step-by-step view of how it works:

1. Setting up an agreement

The business first signs an agreement with a finance provider. Before approving, the provider checks the company’s accounts, its customers, and the type of invoices it issues. This is to make sure the invoices are genuine and that the customers usually pay on time.

2. Issuing invoices

When the business delivers goods or services, it creates an invoice for the customer, often with 30, 60, or 90-day terms. Instead of waiting for the customer to pay, the business also shares this invoice with the finance provider.

3. Invoice verification

The finance provider then verifies the invoice. They check if the details match the order or delivery note and whether the customer has a good history of paying on time. This step usually happens within a day.

4. Advance payment release

After approval, the provider gives an upfront amount to the business normally 70% to 90% of the invoice value. For example, if the invoice is worth $10,000, the business might receive $8,000 within 24–48 hours. This gives the company instant working capital to pay suppliers, salaries, or cover other urgent expenses.

5. Customer makes payment

The customer later pays the invoice as usual, directly to the business. They don’t know that invoice discounting has been used, which helps the company maintain a normal relationship and trust. This is why managing payment invoices correctly is so important it keeps the business finances smooth without affecting the client experience.

6. Final settlement

Once the customer clears the full invoice amount, the business then settles accounts with the finance provider. The remaining balance (after deducting service fees) is released back to the business. For instance, if the provider kept $200 as their fee, the company would get the final $1,800 from the earlier example.

Key Benefits of Invoice Discounting

Invoice discounting helps businesses manage their cash flow, meet financial obligations on time, and plan for steady growth. By understanding these benefits, business owners can use this tool to make their operations smoother and more predictable.

1. Quick Access to Cash

With invoice discounting, businesses can get money from unpaid invoices without waiting for customers to pay. This means they can cover essential expenses like salaries, supplier bills, or utility costs without delays.

Example: A small manufacturer delivers products worth $10,000. Instead of waiting weeks for the customer to pay, the business can receive most of the amount immediately through invoice discounting, keeping operations running smoothly.

2. Smooth Cash Flow

Having cash available when needed helps businesses plan and manage daily operations more effectively. It reduces stress caused by unexpected expenses or delays in customer payments. Using an invoice tracker, business owners can see which invoices are already paid, which are pending, and which ones have been discounted. This clear view makes cash flow planning simple and organized.

3. No Extra Debt

Invoice discounting is not a loan; it uses money that the business has already earned. This keeps financial records clean and avoids adding long-term liabilities. Businesses can maintain stability without worrying about interest rates or repayment schedules.

4. Flexibility for Growth

As a business grows, it generates more invoices. Invoice discounting grows with the business naturally, giving access to more funds when needed. This is especially helpful during busy periods or when the company wants to invest in new opportunities.

Example: A retail shop increases stock for the holiday season. By discounting invoices, it has enough cash to buy extra products and meet high customer demand without waiting for payments from previous orders.

5. Timely Payments to Suppliers and Staff

Quick access to funds ensures suppliers and employees get paid on time. This builds stronger relationships with vendors and staff. In some cases, suppliers may offer discounts for early payment, helping businesses save money.

6. Protects Customer Relationships

Customers continue paying invoices in the usual way, without knowing the invoices were discounted. This helps maintain trust and avoids any negative impact on business relationships.

7. Manage Seasonal Changes Easily

Businesses often face periods of high and low sales. Invoice discounting provides flexibility to handle busy seasons with more funds and manage quieter periods without financial stress. This keeps operations stable throughout the year.

8. Supports Expansion and Investment

Access to fast cash allows businesses to invest in growth, such as buying new equipment, marketing campaigns, or entering new markets, without waiting for customers to pay their invoices.

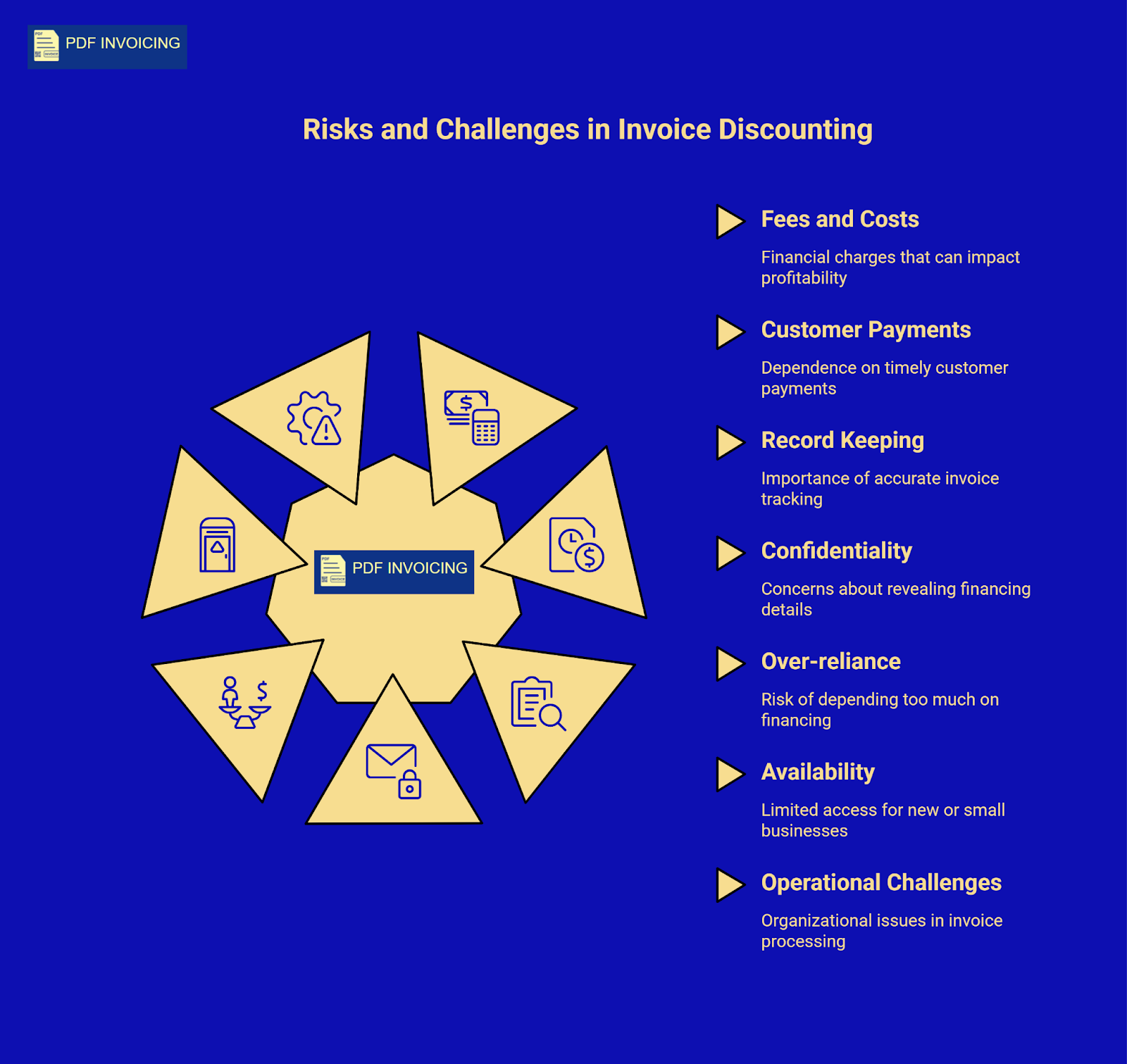

Risks and Challenges of Invoice Discounting

While invoice discounting offers many benefits, businesses also face some risks and challenges. Understanding these can help you manage them proactively and get the most value from this financing option.

1. Fees and Costs

Finance providers charge a fee for their services, usually a small percentage of the invoice value. If not managed carefully, these costs can add up and reduce overall profit. Businesses should compare providers and understand all charges before entering an agreement.

2. Dependence on Customer Payments

Since invoice discounting relies on your customers paying their invoices, any delays or defaults can create problems. If customers take longer than expected to pay, the business may face cash flow pressure despite having advanced funds.

3. Maintaining Accurate Records

Using invoice discounting requires careful tracking of invoices. Mistakes in documentation or mismanagement of an invoice tracker can lead to confusion, delayed payments, or disputes with the finance provider. Keeping accurate records is essential for smooth operations.

4. Confidentiality Concerns

Although most invoice discounting arrangements keep customers unaware, mistakes in communication can reveal the financing. If clients find out, it could affect trust or negotiations. Businesses must handle all documents and correspondence carefully.

5. Over-reliance on Financing

Relying too heavily on invoice discounting may reduce focus on proper cash flow management. It should complement, not replace, good financial planning. Businesses still need to monitor income and expenses to maintain stability.

6. Limited Availability for Some Businesses

New or very small businesses with few invoices or clients may find it difficult to get financing through invoice discounting. Providers typically prefer businesses with a steady flow of invoices from reliable customers.

7. Operational Challenges

The process of submitting invoices, verifying them, and settling with the finance provider requires organization. Without proper systems, it can become time-consuming or error-prone.

Invoice Discounting vs. Other Financing Methods

Invoice discounting is one way to get money fast, but businesses also use loans, overdrafts, or invoice factoring. Each has pros and cons. The table below shows the main differences:

|

Feature |

Invoice Discounting |

Invoice Factoring |

Bank Loan |

Overdraft |

|

How You Get Money |

Advance on your unpaid invoices |

Sell invoices to finance company |

Bank gives you new money |

Bank lets you spend more than your balance |

|

Do You Take Debt? |

No |

No (but provider owns invoices) |

Yes |

Yes, pay interest |

|

Customer Knows? |

Usually no |

Often yes |

Not applicable |

Not applicable |

|

Speed |

Fast, within days |

Fast, but slower than discounting |

Can take weeks |

Immediate if approved |

|

Cost |

Small fee |

Slightly higher fee |

Interest & fees |

Interest on extra amount used |

|

Who Collects Payments |

Business collects |

Finance company collects |

Business collects |

Business collects |

|

Best For |

Quick cash without affecting customers |

Want help collecting money |

Need big, long-term money |

Short-term cash needs |

Are you waiting weeks for your clients to pay, making it hard to manage your business?

Salaries, supplier bills, and day-to-day expenses still need attention, even when payments are delayed. With PDF Invoicing, you can generate, track, and organize all your invoices in one place, access funds faster, and keep your cash flow consistent. This helps you focus on growing your business instead of worrying about late payments.

Conclusion

Invoice discounting is an effective way for businesses to access money stuck in unpaid invoices. This helps companies maintain smooth cash flow, pay suppliers and staff on time, and plan for growth without taking on additional debt. While there are some risks, understanding the process and managing it carefully makes it a practical solution for businesses dealing with late client payments or seasonal cash flow challenges.

Using the right invoicing tools can make the process much easier. By keeping invoices organized, tracking payments clearly, and maintaining accurate records, businesses can ensure the discounting process runs smoothly, reduce errors, and stay in control of their finances. Combining careful financial management with invoice discounting allows companies to focus on growth and confidently handle day-to-day business expenses.

Frequently Asked Questions

1. Is invoice discounting regulated?

Yes, invoice discounting is usually regulated by financial authorities in most countries. The finance providers who offer this service must follow rules to protect businesses and ensure transparency. These regulations cover how fees are charged, how customer data is handled, and how agreements are structured. It gives businesses confidence that the process is safe and fair.

2. How do I discount an invoice?

Discounting an invoice is simple: first, you deliver your product or service and issue the invoice to your customer. Then, you share that invoice with a finance provider. The provider checks the invoice details and approves it. After approval, they pay you most of the invoice value right away. When the customer pays the full amount, the provider keeps a small fee and returns the remaining balance. Many businesses use e-invoicing software to make this process faster and more organized.

3. What is another name for invoice discounting?

Invoice discounting is sometimes also called “invoice financing” or “receivables financing.” These terms all mean that a business can get money from unpaid invoices before the customer actually pays, helping improve cash flow without taking a traditional loan.